Cutler Commentary

Cutler Second Quarter 2026 Market Commentary

July 09, 2026

Investors entered this quarter with plenty to worry about. Midterm election years have a reputation for treating stocks roughly. Oil-price spikes from geopolitical events have a strong track record of preceding recessions.

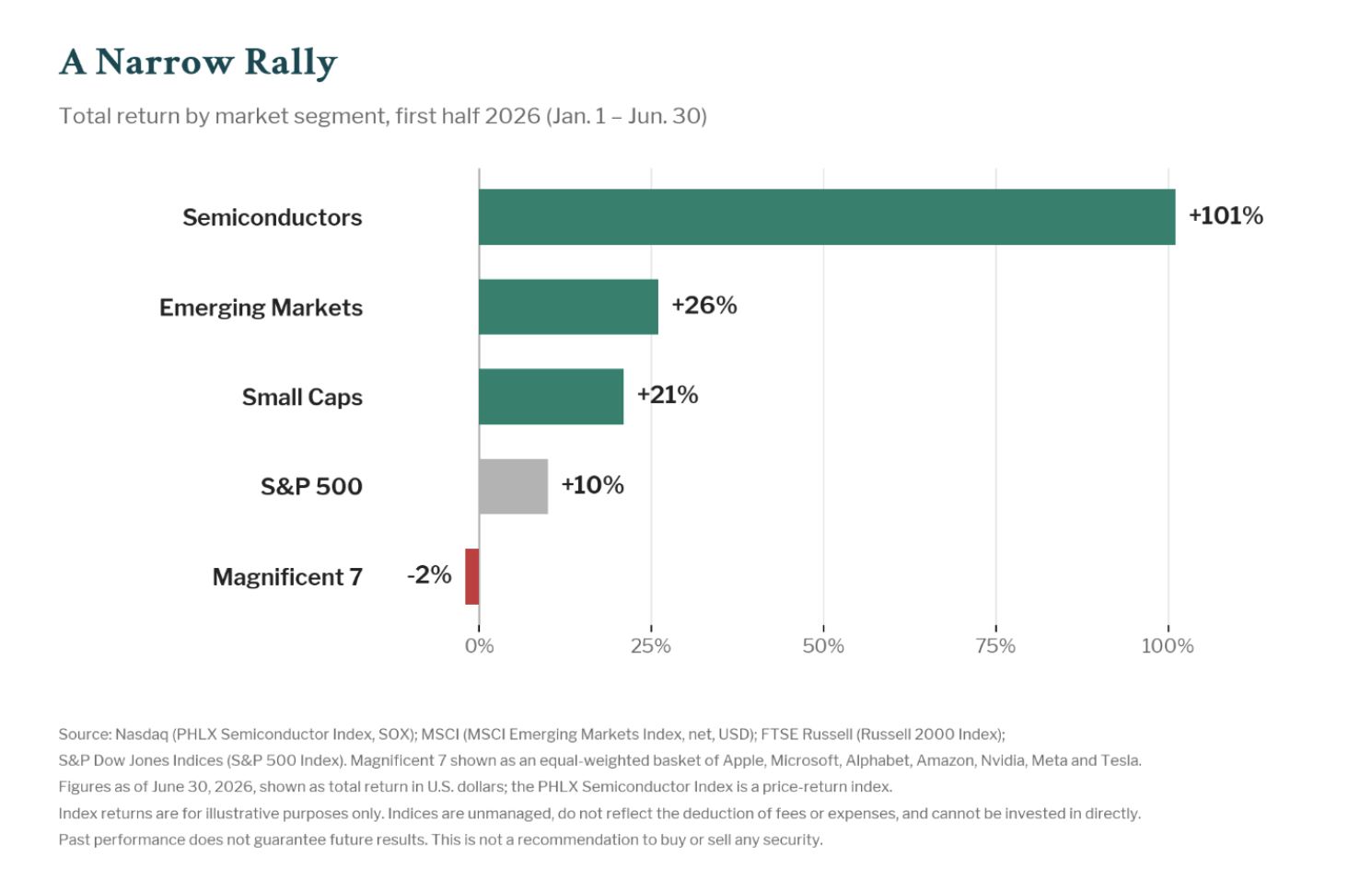

The expression "Don't fight the Fed" has been a warning to not own stocks when rates are rising. Kevin Warsh, the newly installed Fed Chair, has abruptly pivoted the Fed’s rhetoric to one that implies potential tighter monetary policy going forward. And yet, despite these headwinds, the S&P 500 Index rallied 14.9% in the second quarter – the best second quarter in a midterm election year on record. Year-to-date, the broad index’s total return performance now sits at 10.19% through quarter-end.

The rally was not confined to large U.S. companies. Small-cap stocks, as measured by the Russell 2000 Index, are outperforming even more, at about 20% year-to-date. Non-U.S. equities have rallied as well, especially those in emerging markets. Notably, the KOSPI Composite, which tracks South Korean stocks and is heavily exposed to memory-chip manufacturing, has risen more than 100% in local currency terms in the first half of the year.

There is only one explanation for the market's continued strength: the artificial-intelligence trade remains in full swing. What changed in the second quarter, however, was its leadership. Apart from Alphabet, the other Magnificent Seven "hyperscalers" have underperformed the S&P 500, and the outperformance has instead been concentrated in semiconductor manufacturers. According to Barclays, chip and computer-hardware stocks accounted for roughly 87% of the market advance in the first half of 2026. Semiconductor manufacturers, which have rallied around 101% thus far in 2026, now represent a record 19% of the S&P 500 (NVIDIA remains the world's most valuable company), with the technology sector overall a remarkable 39% of the US stock market. Memory chip makers such as SanDisk and Micron were standouts of the chip rally, up 860% and 304% respectively since the beginning of the year.

It is important to note that these stock prices are not being driven higher by speculation. Unlike the dot com bubble of the late 1990s, this rally is underwritten by real earnings, with year-over-year gains estimated at 23.3% for the second quarter, according to FactSet. The AI capital-investment cycle has produced real profits up and down the supply chain, from data-center construction to the chips and components doing the actual computing. Even so, cautious investors are right to ask how long those earnings can last. For now, the buildout has handed chipmakers extraordinary pricing power. Apple CEO Tim Cook recently acknowledged that memory-driven price increases had become "unavoidable" as the company raised prices on certain MacBook and iPad models, and industry analysts expect the memory shortage to persist well into 2027. This suggests pricing power will likely persist in the near term. Beyond the anticipated earnings growth of the next year or two, however, investors may want to proceed carefully as they seek to capitalize on today’s “gold rush.”

One other event during the quarter caught our collective attention. Space Exploration Technologies (SpaceX) went public in the largest IPO in U.S. market history, debuting at roughly a $2 trillion valuation amid seemingly insatiable retail demand. Much of that enthusiasm reflects Elon Musk's track record for innovation, along with SpaceX's near-monopoly on launching payloads into space and, through Starlink, on satellite-based internet. The risks, however, are just as outsized: this is a stock with a valuation in a league of its own. For Cutler’s clients, what the IPO signals matters more than any return this single stock might deliver. After a long drought, the door for new public companies has swung back open, with other marquee names such as Anthropic and OpenAI reportedly preparing to follow. While this may indicate a renewed willingness from investors to take on risk, a rush to invest in IPOs are yet another example of the exuberant risk appetite of today’s investors. Even with this exuberant market sentiment, we remain constructive on the AI buildout and equities over the long term, provided investors stay disciplined.

Will AI be a strong enough thesis to overcome today’s headwinds? With risks abundant but risk-taking still being rewarded, our advice remains the same: stay diversified. Diversification beyond the S&P 500 is working. This approach spreads risks across multiple asset classes and is intended to smooth returns over time. In an environment where returns for the S&P 500 are attributed to just a handful of securities, possessing portfolio contributions from a variety of asset classes has multiple benefits. We continue to maintain our core philosophies at Cutler grounded in income, diversification, and valuations. Today’s investors should be well-served by maintaining these disciplines and adhering to a process focused on their investment goals.

Past performance is not indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable or suitable for a particular investor's financial situation or risk tolerance. Investing involves risk, including loss of principal. You cannot invest directly in an index. Asset allocation and portfolio diversification cannot assure or guarantee better performance and cannot eliminate the risk of investment losses.

The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. The Russell 2000 Index measures the performance of the approximately 2,000 smallest companies in the Russell 3000 Index and is a widely used gauge of U.S. small-capitalization equities. The PHLX Semiconductor Index (SOX) is a modified market capitalization weighted index composed of companies primarily engaged in the design, distribution, manufacture, and sale of semiconductors; it is a price return index and does not reflect the reinvestment of dividends. The MSCI Emerging Markets Index captures large- and mid-capitalization representation across emerging markets countries and is presented on a net total return basis in U.S. dollars. The KOSPI Composite Index is a market capitalization weighted index of all common stocks listed on the Korea Exchange and is denominated in Korean won. The "Magnificent 7" is not an index and is represented as an equal-weighted basket of Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, and Tesla, constructed for illustrative purposes and not available for direct investment. These indices do not incorporate Environmental, Social, or Governance (ESG) criteria.

All opinions and data included in this commentary are as of June 30, 2026, and are subject to change. The opinions and views expressed herein are of Cutler Investment Counsel, LLC and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This report is provided for informational purposes only and should not be considered a recommendation or solicitation to purchase securities. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither Cutler Investment Counsel, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

CATEGORIES

Disclaimer

These blogs are provided for informational purposes only and represent Cutler Investment Group’s (“Cutler”) views as of the date of posting. Such views are subject to change at any point without notice. The information in the blogs should not be considered investment advice or a recommendation to buy or sell any types of securities. Some of the information provided has been obtained from third party sources believed to be reliable but such information is not guaranteed. Cutler has not taken into account the investment objectives, financial situation or particular needs of any individual investor. There is a risk of loss from an investment in securities, including the risk of loss of principal. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor's financial situation or risk tolerance. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary. No reliance should be placed on, and no guarantee should be assumed from, any such statements or forecasts when making any investment decision.